Roadmap for alternative energy - Australian mining

- Marc Allen

- Nov 25, 2019

- 7 min read

Below is a reprint of my extended abstract for a paper I presented at the AusIMM Future Mining conference in Sydney last week. You can also download the presentation material here.

INTRODUCTION

Globally, the outputs of the mining and mineral processing industry are, and will continue to be, critical for the progression of society. Demand for some metals and minerals such as copper, nickel, lithium, rare earths, silicon, potash and many others will increase markedly in coming years to support societal progress. However, drivers such as the global transition to a net-zero emissions circular economy combined with increasing energy costs and risks associated with global climate change action are causing miners to rethink the way in which mines and mineral processing operations receive, generate and use energy across their entire operation. The Paris Agreement, set in 2015 and signed/ratified in 2016, sets a goal of a global temperature increase of “well below 2°C above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5°C above pre-industrial levels”. In practice, this will require global emissions to be net zero (i.e., sinks that remove CO2 from the atmosphere are equal to sources that emit CO2 into the atmosphere) in the latter half of the century – between 2050 and 2070. Long term, the mining and mineral processing industry will also need to be net zero emissions in this timeframe.

To explore alternative energy supply options that support these long-term goals, the mining value chain has been split into different areas and the potential alternative energies available. Mining processes are considered, both underground and open pit, including mobile and fixed equipment. Mineral processing is then also discussed, both hydro- and pyro-metallurgical.

MINING PROCESSES

For open-pit mines, the main energy user is the mobile fleet – generally very large haul trucks, excavators, drills, loaders and other large mobile equipment. Invariably, this equipment is powered by diesel, which has the advantage of being readily available with strong supply chains and having a high energy density by volume (energy per unit of fuel). Diesel however is a relatively expensive fuel source and relatively high emissions intensity compared to other fuel sources. For underground mines, the equipment used is similar, but necessarily smaller – given the nature of operations. Underground mining has an additional large energy consumer in the ventilation and water pumping operations. These are powered by mine site electricity.

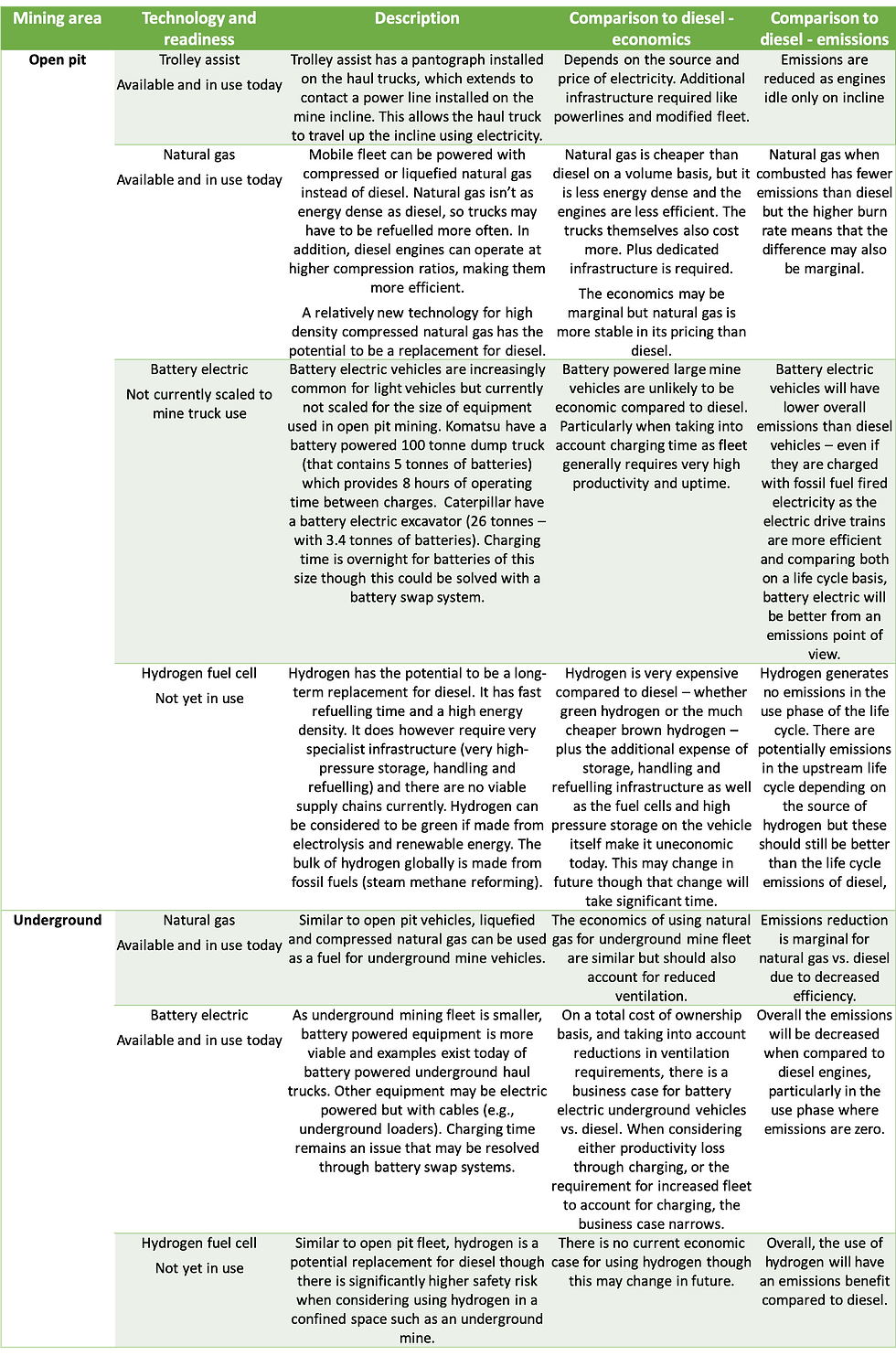

Taking the view that alternative energy for mine fleet should be economic and support the longer-term goal of low emissions mining, the following technologies could be applied. The table below shows the different alternative energy technologies for open pit and underground mine fleet, the technology level today, relative economics compared to diesel and the relative ability to support a lower emissions goal.

TABLE 1 – Summary of alternative energy technologies for mining

From the above table, it is clear that there is some way to go to progress low emissions vehicles in the mining industry – particularly for the larger equipment used in open pit mining. Battery electric vehicles, while showing some promise in the underground mining area, still is disadvantaged somewhat by the charge times required. If large advancements are made in rapid charging infrastructure then some of these issues may be resolved and help to progress the uptake of this technology through the industry. Both trolley assist for open pit mining and the use of natural gas can be implemented now. Trolley assist is a mature technology that will act to reduce costs and emissions. The case for natural gas is more marginal currently but may be favoured by reducing volatility in fuel pricing.

Finally hydrogen, whilst receiving a lot of attention currently, is many years from being viable. There are a number of technical challenges with storage, compression and use – and there is no viable supply chain currently. This is an area to watch but not seen as a serious contender in the medium term. It is however, the best forthcoming alternative for large vehicles such as those used in open pit mining – particularly from an emissions point of view.

MINERAL PROCESSING

Mineral processing requirements for energy can effectively be split into requirements for low grade heat, high grade heat and electricity. Generally, hydrometallurgical operations use electricity for most plant energy needs, with potentially a small amount of low grade heat. Pyrometallurgical processes require high grade heat.

The best option for supplying low grade heat is to electrify the heat source. That is, use electricity to supply energy to boilers and or furnaces to transfer heat to a heating medium (hot water or hot oil). In global decarbonisation efforts, the first step is to electrify everything that can be electrified and then decarbonise the electricity supply.

For the electricity supply, lower emissions and zero emissions electricity is becoming commonplace. Solar PV at utility scale and onshore wind both compare favourably on a levelized cost of energy basis to even coal fired power and certain jurisdictions are getting close to the time where the cost of new build solar PV and onshore wind will be cheaper than the operating cost of black coal fired power. The vast majority of mine site power, particularly in Australia, comes from diesel fired power generation. In these cases, there is an economic case to install solar and/or wind (depending on the resource) and justify that expenditure based on diesel fuel savings alone. Since this economic case exists, the challenge now is to account for the intermittent nature of renewable power generation by providing back up or energy storage. The most cost effective solution for a site that is currently diesel powered is to continue to use that diesel fired power station as the way to firm that renewable power generation.

Significant advancements in microgrid control have been made in recent years and also in the prediction technology for wind and solar. This makes a hybrid integrated system a distinct possibility for mine sites today – and it has been demonstrated in some sites in Australia, notably the Sandfire Resources Degrussa copper project. For projects with proximity to a gas supply or to a liquefied natural gas supply chain, using gas fired power generation has the potential to save costs and emissions compared to diesel.

The alternative to providing backup from traditional power generation is to use energy storage of some description. Battery storage with lithium ion batteries is a good way to provide short term storage as part of a hybrid renewables-fossil fuel system and to reduce the amount of spinning reserve in the fossil fuel fired power generation. These may not be the most appropriate for large storage however as lithium ion tends to be good for discharging over short time periods. Large lithium ion battery banks such as the one in South Australia at the Hornsdale Power Reserve are just a series of smaller battery banks so the capital cost increases relatively linearly as more and more capacity is added. The figure below shows the applicability of different types of energy storage.

FIGURE 1 – Energy storage technology and applicability

For storage on a mine site, which may require long discharge times and high capacity, other options such as physical storage (pumped hydro, compressed air, cryogenic) or chemical storage such as redox flow batteries, hydrogen or methane may be more appropriate. The other thing to take into account, if there’s a desire to have no fossil fuel back up at all is that a renewable power plant must be oversized much higher than the demand to allow for excess power to go into the storage.

For high grade heat, there aren’t many viable options today and this is considered to be one of the more difficult areas to decarbonise. Hydrogen is tipped as the long term replacement for natural gas for supply of industrial heat and for use in smelters, blast furnaces etc. though this has a long way to go in terms of economics and technical challenges. Solar thermal power plants, which may offer a solution in terms of 24 x 7 solar power generation do also generate heat at about 300°C – not quite enough for a smelter or other pyrometallurgical processes but could solve the intermittency problems for power generation.

Overall, the most promising alternative energy technology for mineral processing is the use of hybrid systems consisting of solar or wind with a traditional fossil fuel backup and a small amount of battery storage to link the two and reduce spinning reserve. Other technologies are in their infancy or currently not economic. To truly get to zero emissions in an off-grid context or an islanded grid will require significant investment in larger power generation capacity and storage so this is considered to be a long-term option for the industry. It will need to wait until storage technology is sufficiently advanced and cost effective – and will not necessarily be lithium ion battery storage is this isn’t so effective for high power discharge over a long time.

CONCLUSIONS

There are technologies today to help decarbonise the mining and mineral processing industry though it will be some time before the industry can get to net-zero emissions, and this may still involve the use of significant offsets rather than being zero absolute emissions. For mining operations, the use of trolley assist and natural gas will provide a relatively quick win with existing technology. Longer term, the industry should be looking towards battery electric for underground and hydrogen for open pit (very long term).

For mineral processing, the decarbonisation challenge is all about electricity supply. Alternatives exist currently for hybrid systems combining renewables from solar PV or wind with traditional diesel or gas fired generation, with a battery system to reduce spinning reserve. This is in use today at a small number of mine sites globally. Longer term, advances in storage technology still need to be made to make a renewables powered off-grid power supply cost effective. High grade heat and smelting processes will continue to be difficult to decarbonise and will potentially have to wait until hydrogen is cost effective before it is used widely.

Comments